Corporate Restructuring according to the Debtor Rehabilitation and Bankruptcy Act (DRBA)

A. Introduction

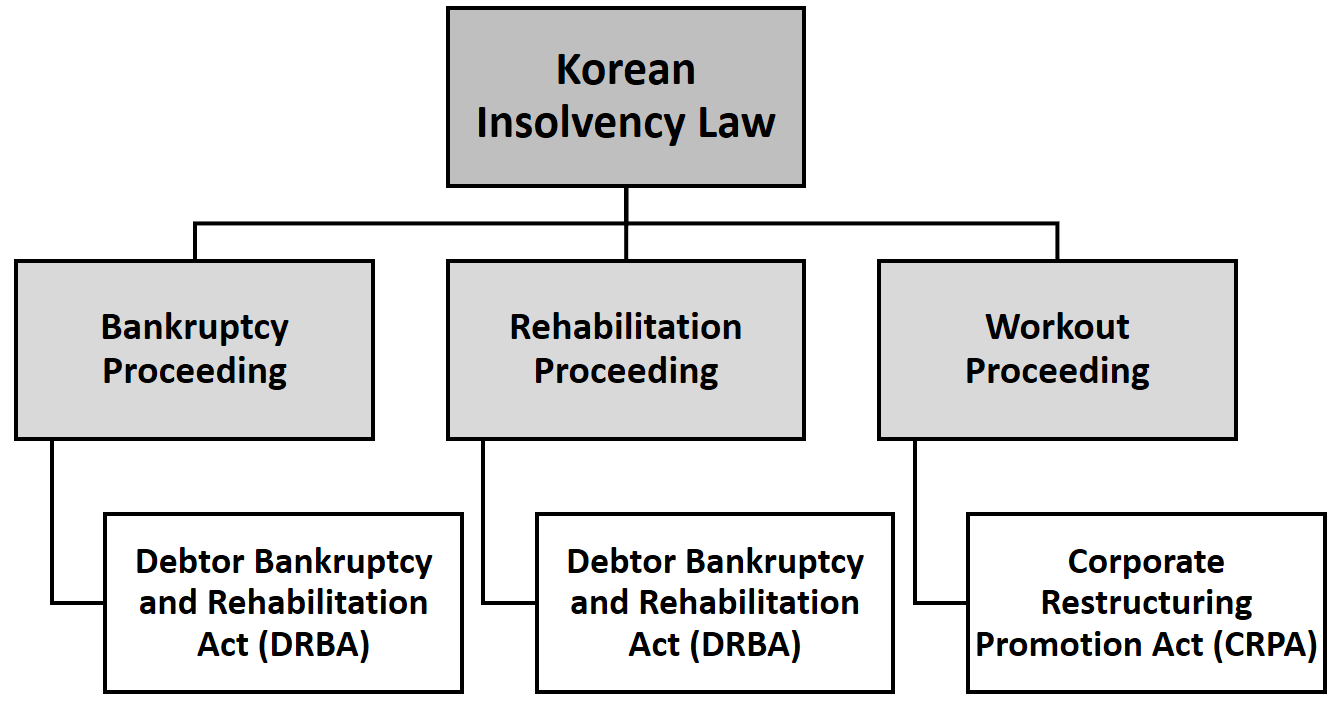

Under Korean insolvency law, there are three available proceedings: the bankruptcy proceeding (under the DRBA), the rehabilitation proceeding (also under the DRBA) and the workout proceeding (under the CRPA).

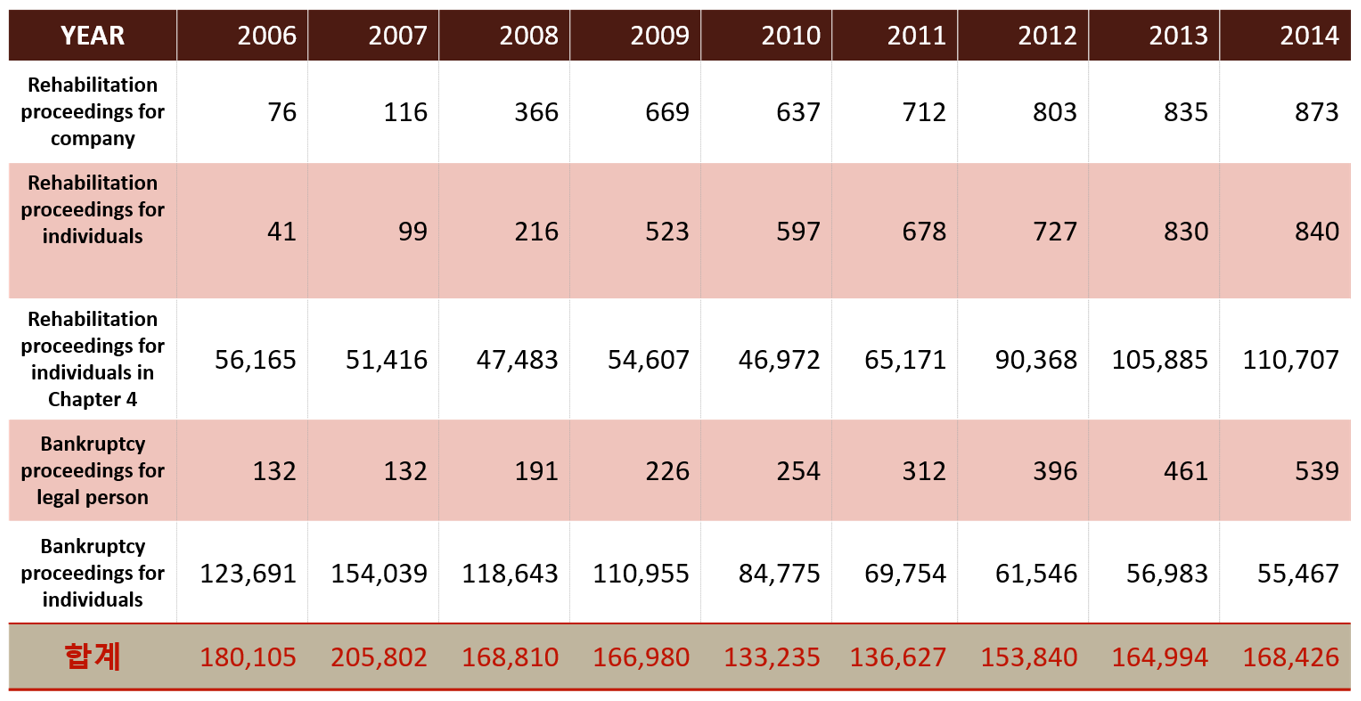

This figure shows the development of the number of the different proceedings. It is obvious that over the years since 2006 the number of rehabilitation proceedings have been increasing faster than the number of the bankruptcy proceedings. It is a fact that the rehabilitation proceeding is getting more popular and especially more important. The reason for that lies in the advantages of these rehabilitation proceedings.

B. Purpose

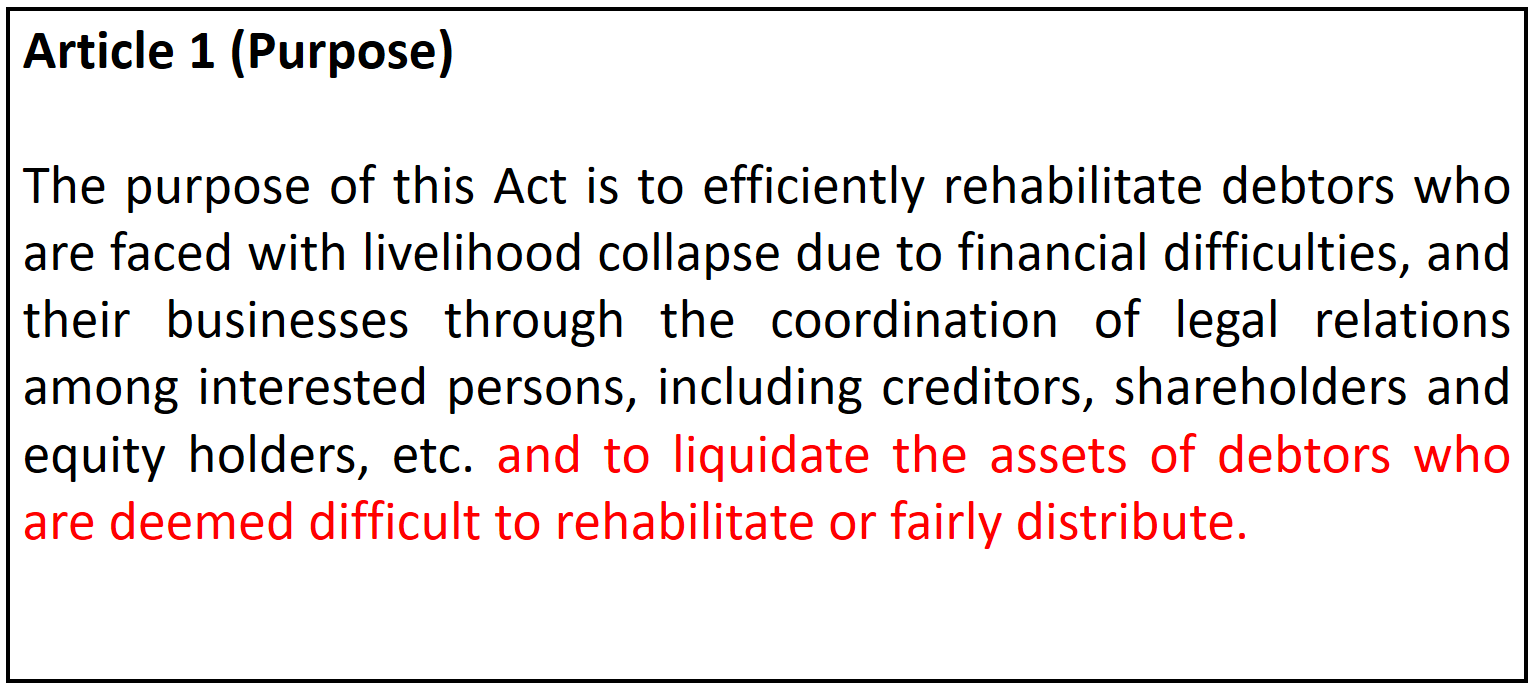

The purpose of the „Debtor Rehabilitation and Bankruptcy Act“ is determined in Article 1 of this Act. It says: „The purpose of this Act is to efficiently rehabilitate debtors who are faced with livelihood collapse due to financial difficulties, and their businesses through the coordination of legal relations among interested persons, including creditors, shareholders and equity holders, etc. and to liquidate the assets of debtors who are deemed difficult to rehabilitate of fairly distribute.“So the first, black colored, part is relating to the rehabilitation proceedings while the orange colored part is relating to the bankruptcy proceedings. There is another really important thing here: The purpose of the DRBA already shows, that there is some kind of hierarchy or priority of the proceedings. The rehabilitation proceeding is the first priority and the bankruptcy is the second priority. At first, a rehabilitation proceeding hast o be tried. Only if the rehabilitation proceeding is not possible or if the debtor is deemed difficult to rehabilitate or fairly distribute, the rehabilitation proceeding can be left and the bankruptcy proceeding can be commenced.

C. Advantages

Debtor maintains control of the company

One big advantage of a rehabilitation proceeding (especially for the debtor) is, that the management maintains the control of the company. Article 74 of the Debtor Rehabilitation and Bankruptcy Act has adopted a system (that is also known as DIP, so Debtor in Possession, in the American bankruptcy law), where the management of the debtor company becomes the custodian under the rationale that the management may actively utilize the corporate rehabilitation procedure as well as the management’s know-how to increase the efficiency of the proceeding itself. However, the management may not maintain control in cases of financial ruin arising from misuse of corporate property, mismanagement or upon request by creditor on reasonable grounds.

Suspension of collection and debt forgiveness

According to a submitted 10 year restructuring plan, the debtor may, with the consent of the creditors and under the court’s oversight, pay off the debt in installments. Collection efforts can be suspended and in some cases, the debts can be forgiven.

Prevent bankruptcy

In a rehabilitation proceeding, wage claims and trade payables can, but only with the permission of the responsible court, be paid preferentially to prevent labor disputes and small and medium suppliers from going bankrupt.

Creditors cannot exercise rights individually

Another important advantage of a rehabilitation proceeding is the fact, that creditors cannot exercise rights individually. Once a rehabilitation proceeding commences, the individual exercises of creditors‘ rights such as provisional attachment, provisional injunction, compulsory execution, and enforcement of security rights are suspended or prohibited to allow some breathing room for the debtor.

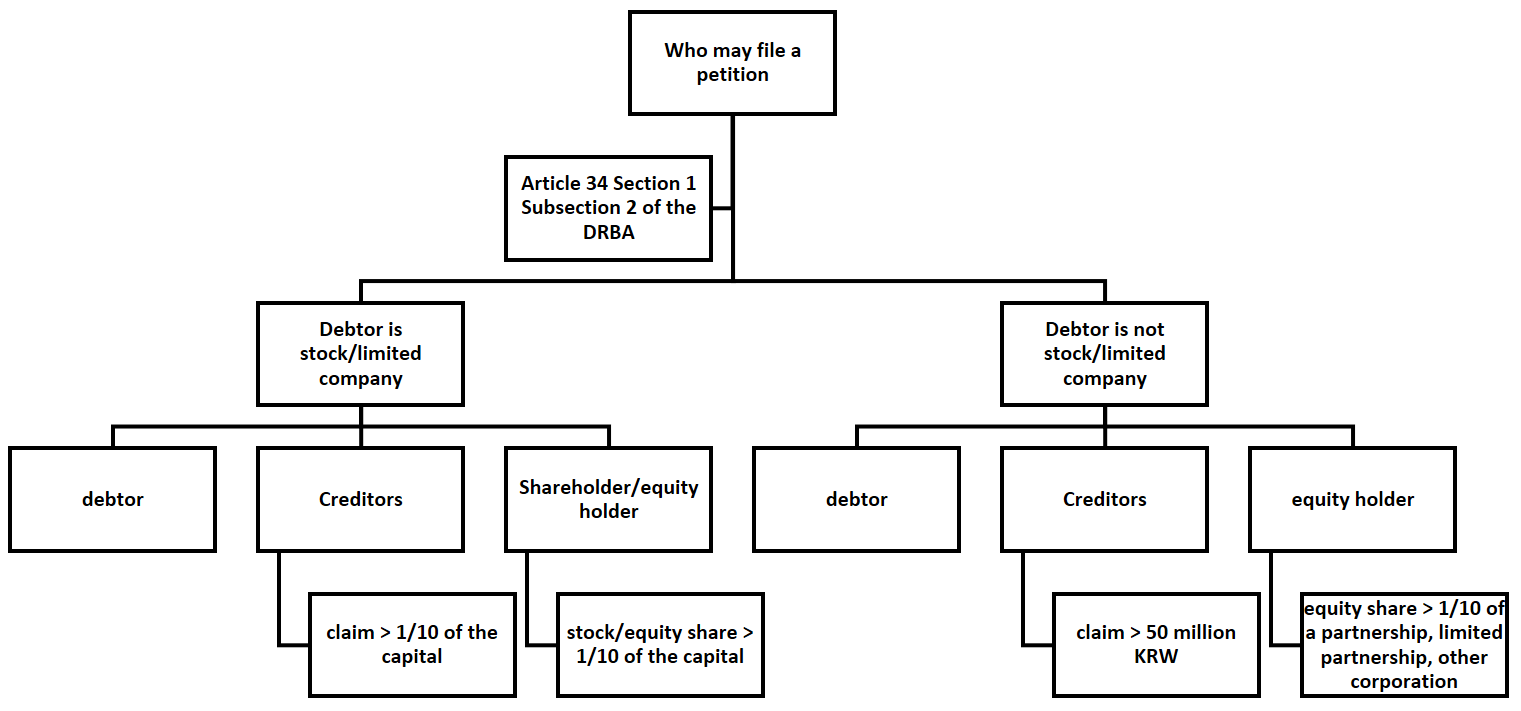

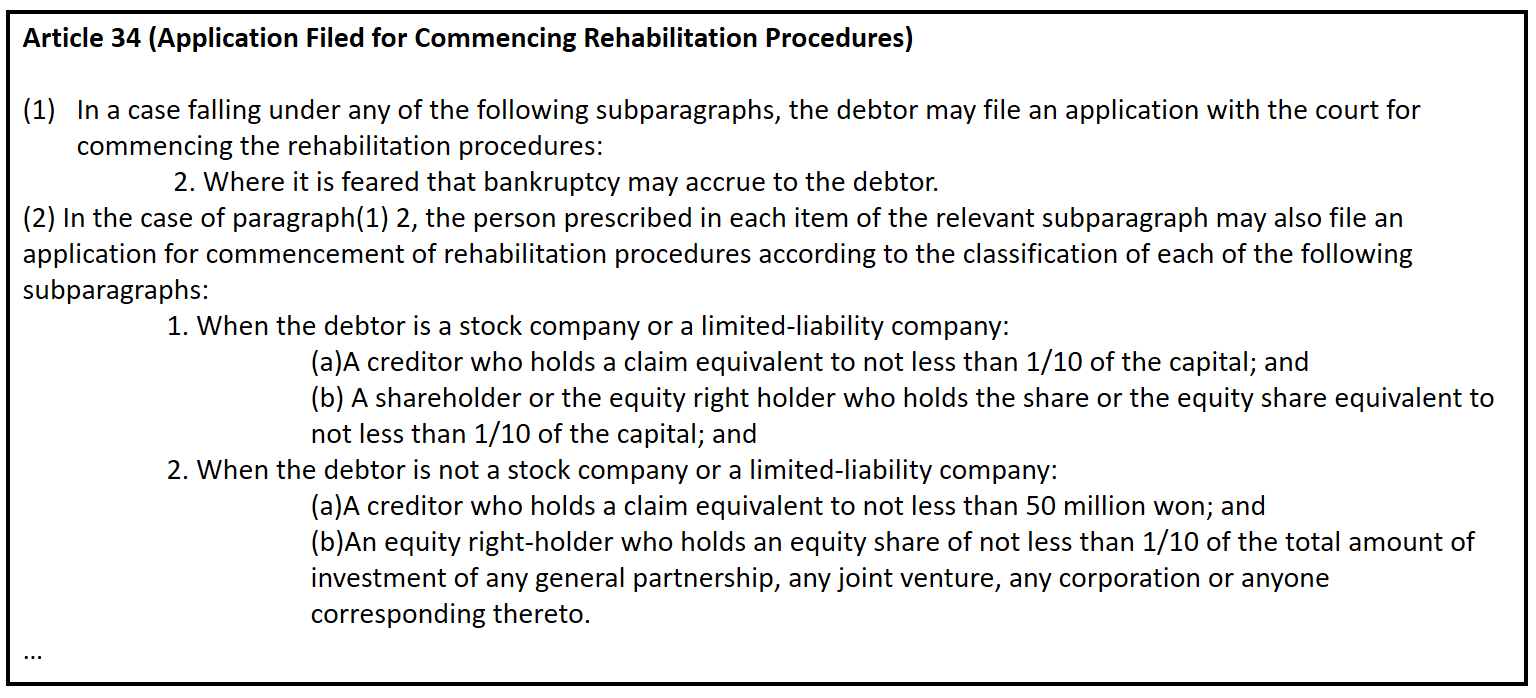

D. Eligibility

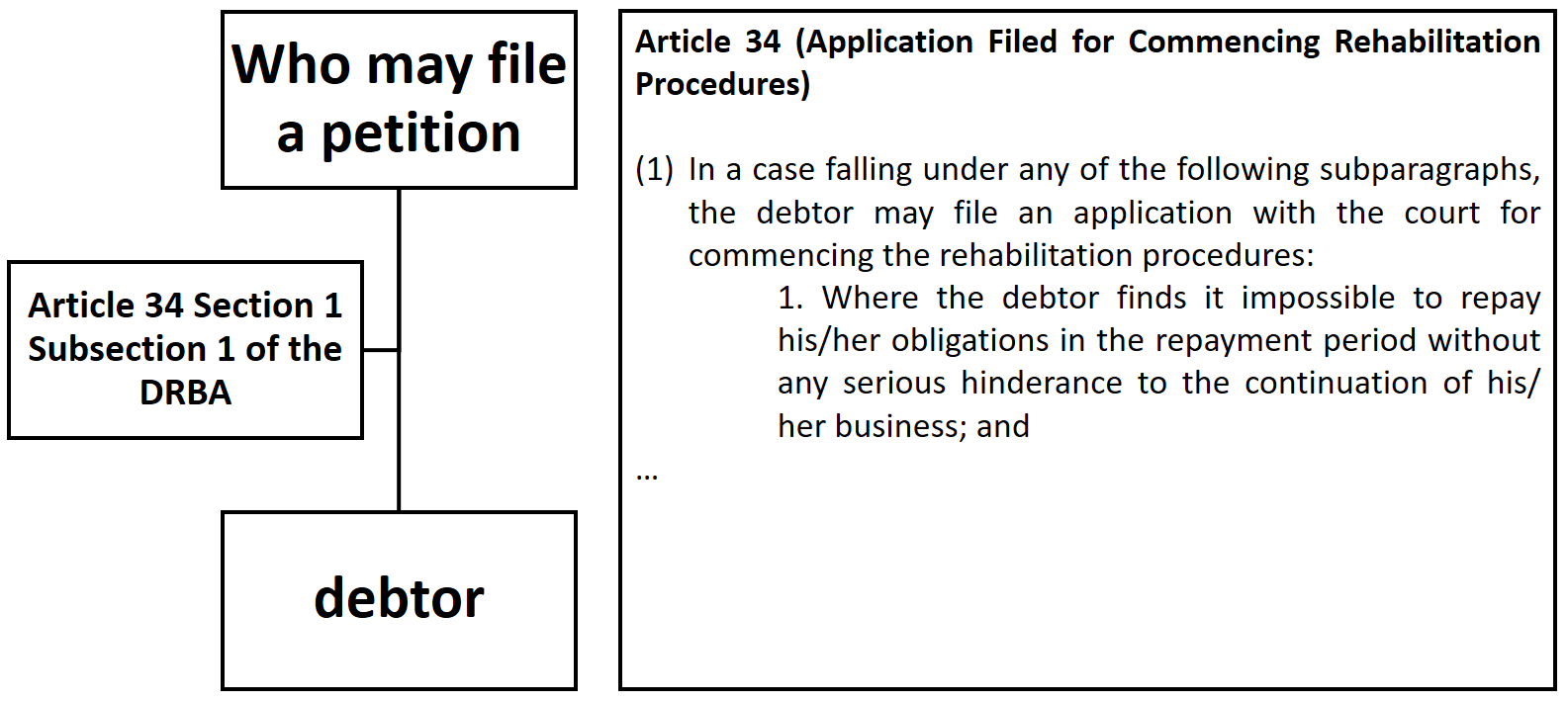

According to Article 34 Section 1 Subsection 1 of the DRBA, the debtor can file a petition where the debtor finds it impossible to repay his/her obligations in the repayment period without any serious hinderance to the continuation of his/her business.

But not only the debtor is able to file a petition. According to Article 34 Section 1 Subsection 2 of the DRBA, it is pivotal whether the debtor is a stock/limited company or not. If the debtor is a stock/limited company, there are three parties, that are able to file a petition: the debtor, the creditors whose claims are equivalent to not less than 1/10 of the capital and shareholder/equity holder whose stock/equity share is equivalent to not less than 1/10 of the capital. If the debtor is not a stock/limited company, there are also three parties who are able to file a petition: the debtor, creditors whose claims are equivalent to not less than 50 million KRW and equity holder whose share is equivalent to not less than 1/10 of a partnership, limited partnership or other corporation.

E. Procedure

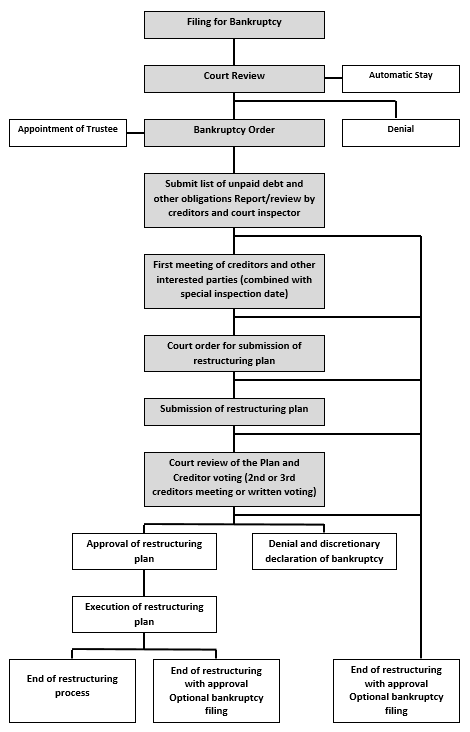

This is a brief overview over the whole procedure. So first, an entitled party has to file for bankruptcy. The court reviews the filing and the case. If it doesn’t withstand the substantial test or if it doesn’t comply with the requirements, the case can be automatically stayed or the court can deny the case. If everything fits, there is a bankruptcy order and the trustee has to be appointed. The debtor submits a list of all unpaid debts and other obligations. This list is reviewed by the creditors and the court inspector. After this, there is the first meeting of creditors and other interested parties. Then, the restructuring plan has to be submitted. After the plan is submitted, the court reviews the plan and the creditors have to vote if they accept this plan. There are more meetings. The votings are by writing. What now happens, depends on the voting. If the majority of the creditors don’t accept the plan, the plan is denied and bankruptcy can be declared. But if they accept the plan, the restructuring plan is approved and executed. But even if the restructuring plan is executed, there is the possibility to optional file for bankruptcy, if the plan doesn’t work. As you can see on the right side, there is, until the list of unpaid debts is submitted, always the possibility to end the restructuring and file for bankruptcy.

© Christoph Bieramperl (2016)